backtest

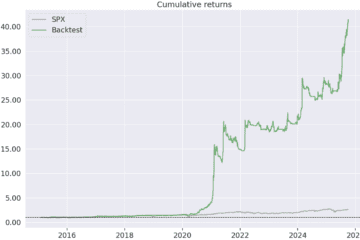

Backtest 92 – Systematic 1D strategy on World indices

Backtest of the systematic World 1D strategy over 7,666 US and European equities on a daily timeframe across roughly 10 years. It produced a 40% CAGR with a 29% max drawdown, 1.79 Sortino and 1.15 Sharpe over 374 trades – backtested, not live, figures.