29% Exposure – 1.66 Sharpe – 32% Max Drawdown (2018-2026)

Most crypto backtests lead with absurd equity curves.

This one doesn’t.

Let’s start with what actually matters:

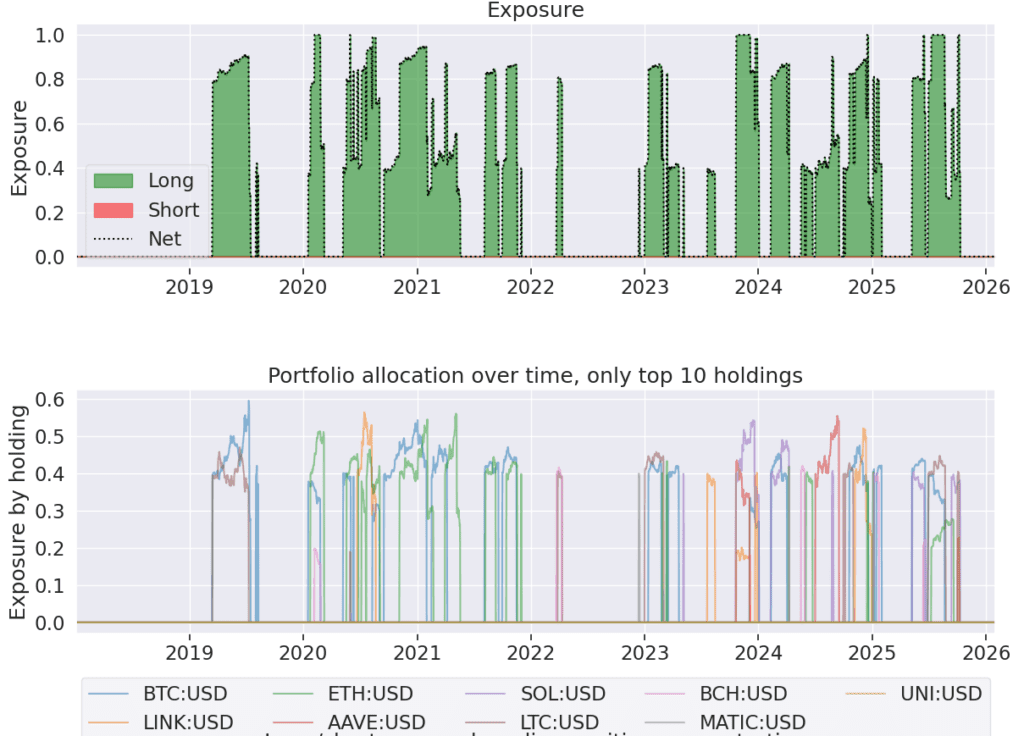

- Net exposure: 29.4%

- Max drawdown: −32.3%

- Sharpe ratio: 1.66

- Calmar ratio: 2.10

- Ulcer index: 5.56%

- Trades: 71 over 8 years

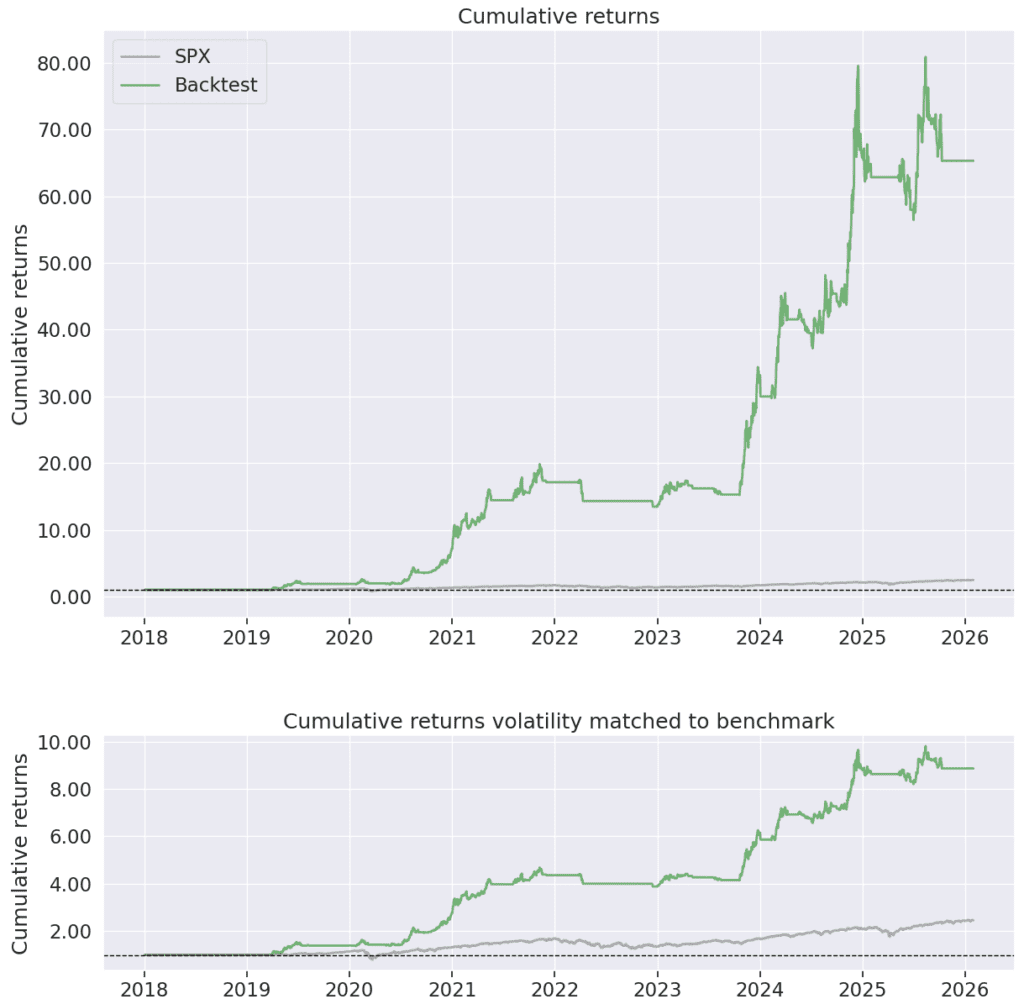

CAGR is 67.7%, but that’s not the point.

The point is return per unit of exposure and drawdown control.

1. Strategy Design Philosophy

This is not a prediction model.

It is a regime participation system designed to:

- Enter volatility expansion phases

- Confirm structural trend alignment

- Exit aggressively when regime deteriorates

- Stay in cash most of the time

Average exposure over 8 years: 29%

It avoids the structural crypto bear phases instead of trying to survive them.

2. Architecture

Entry Layer

- Bollinger-based regime trigger (

bband2a) - Detects volatility compression → expansion

Exit Layer

Ensemble of:

ichimoku6aichimoku5aichimoku4a

Exit logic is deliberately redundant.

Risk Layer

- 32% trailing stop

- No leverage

- Position target: 40%

- Max position cap: 60%

- 7% annual interest on idle cash

Universe:

- 9 liquid USD crypto pairs

- Daily bars

- Long-only

3. Configuration

Strategy Configuration

| Category | Parameter | Value |

|---|---|---|

| Core Setup | Bar Size | 1 Day |

| Universe Size | 9 Crypto Pairs (USD) | |

| Leverage | 1.0 (No leverage) | |

| Initial Capital | $100,000 | |

| Interest on Cash | 7% Annual | |

| Signal Engine | Entry Logic | Bollinger Regime (bband2a) |

| Exit Logic | Ichimoku Ensemble (6a + 5a + 4a) | |

| Scoring Model | Weighted Composite (16 factors) | |

| Freeze Bars | 2 Bars | |

| Risk Management | Trailing Stop | 32% |

| Position Target Weight | 40% | |

| Max Position Weight | 60% | |

| Max Entries per Bar | 10 | |

| Exposure Controls | Exposure Penalty Trigger | 5% |

| Stability Penalty Trigger | 0.30 | |

| Backtest Period | Data Start | 20 Dec 2016 |

| Simulation Start | 02 Jan 2018 – 31 Jan 2026 |

4. Performance Summary (2018-2026)

Initial capital: $100,000

Final equity: $6,531,155

But again, focus on structure:

Performance Summary (2018-2026)

| Metric | Value |

|---|---|

| Final Equity | $6,531,156 |

| Total Return | +6,431% |

| CAGR | 67.74% |

| Max Drawdown | −32.26% |

| Ulcer Index | 5.56% |

| Sharpe Ratio | 1.66 |

| Sortino Ratio | 2.53 |

| Calmar Ratio | 2.10 |

| Stability | 0.935 |

| K-Ratio | 203.41 |

| Net Exposure | 29.40% |

| Trades | 71 |

| Win Rate | 60.56% |

| Risk / Reward | 7.76 |

| Kelly Fraction | 55.48% |

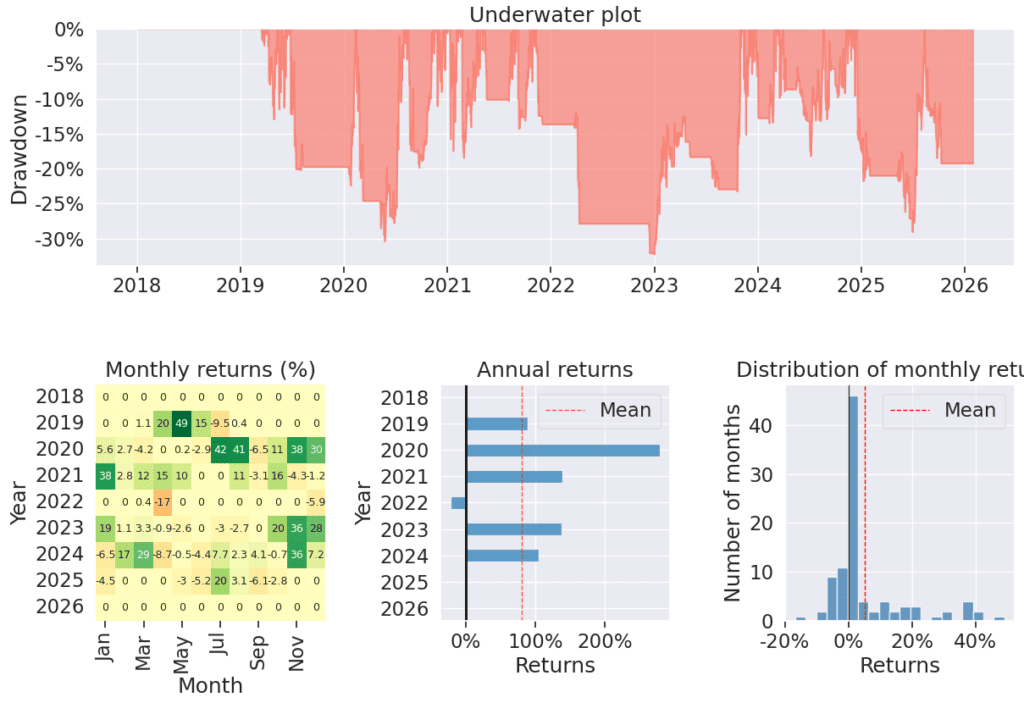

71 trades in 8 years.

This is a slow, selective trend system, not hyperactive trading.

5. Distribution Profile

Trade return distribution:

- Median: +3.0%

- 80th percentile: +54%

- 95th percentile: +192%

- Worst trade: −25.9%

This is clearly positively skewed.

Performance is driven by:

- Few large structural trend captures

- Limited downside per trade

- Strict exit discipline

It does not rely on high win rate.

It relies on asymmetric payoff.

6. Risk Characteristics

Drawdown Profile

Max DD: −32%

In crypto terms, that is materially lower than passive exposure.

More important:

Ulcer index = 5.56%

Meaning drawdowns are not only shallow, but relatively short-lived.

Stability

Stability score: 0.935

K-ratio: 203

The equity curve is statistically smooth relative to asset volatility.

That suggests:

- Regime filtering is doing real work

- Not pure beta harvesting

6. What This Is NOT

Let’s be explicit:

- Not slippage-stress-tested yet

- No liquidity impact modeling

- Universe limited to 9 assets

- Crypto structural bull market tailwind (2020-2021)

- Trailing stop execution on daily bars may overestimate fills

This is research-grade, not audited live performance.

7. Why This Is Interesting

The key metric here is:

67% CAGR at 29% exposure

If exposure were 100%, risk profile would be completely different.

This suggests the system is:

- Efficient at timing participation

- Avoiding large bear regimes

- Capturing convexity phases

That is structurally different from buy-and-hold.

8. What Needs to Be Proven Next

Before considering capital deployment:

- Walk-forward optimization

- Parameter perturbation test (±20% sensitivity)

- Slippage stress test (0.1-0.5%)

- Sub-universe validation

- Post-2024 strict out-of-sample monitoring

- Exposure cap reduction to 20% to test robustness

If performance collapses under minor perturbations, edge is fragile.

If not, we may have something durable.

9. Bottom Line

This is not about turning $100k into $6M.

It’s about:

- Controlled participation

- Positive skew

- Low exposure efficiency

- Stable equity compounding

The next step is robustness validation – not marketing.

Out-of-sample cutoff. This strategy’s rules and parameters were frozen on 3 July 2025. All performance shown after that date is genuine out-of-sample / forward-tracked data – it post-dates the freeze, so no hindsight or selection could have shaped the rules.

This is a historical backtest, published for informational and educational purposes only – not financial advice, not a recommendation, and not a trading signal. Past performance is not indicative of future results.

Backtest output and ongoing research:

→ Community channels

→ https://x.com/kreamedge

See the discussion on X/Twitter.

0 Comments