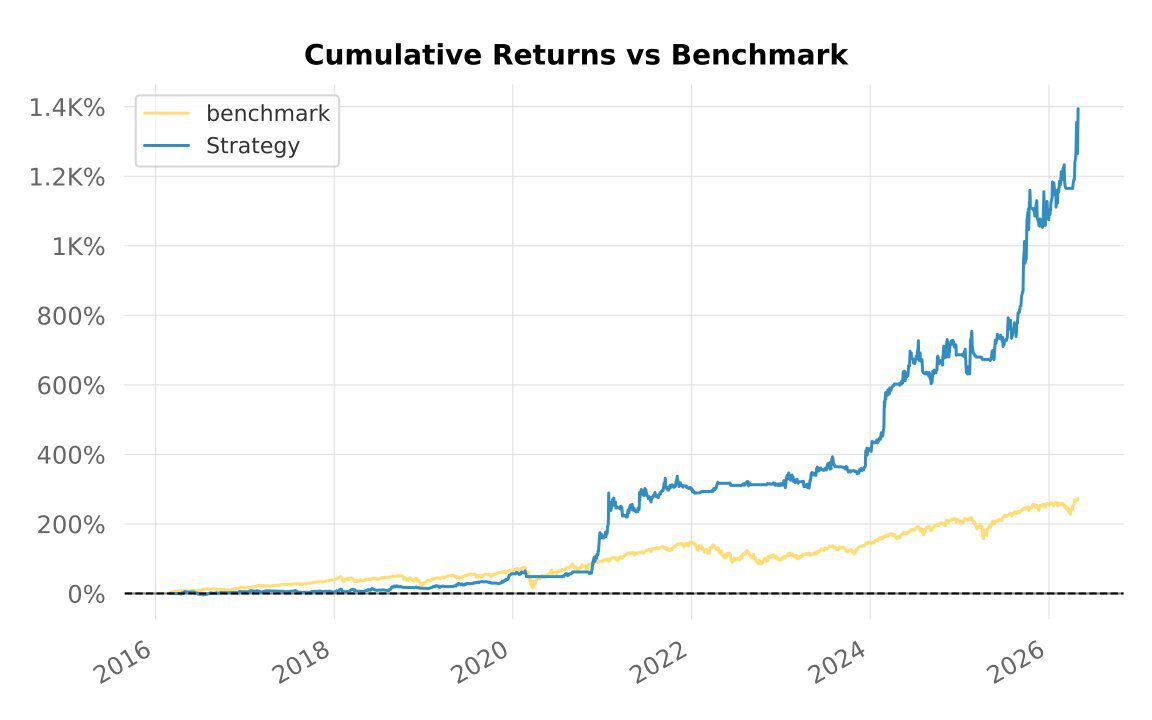

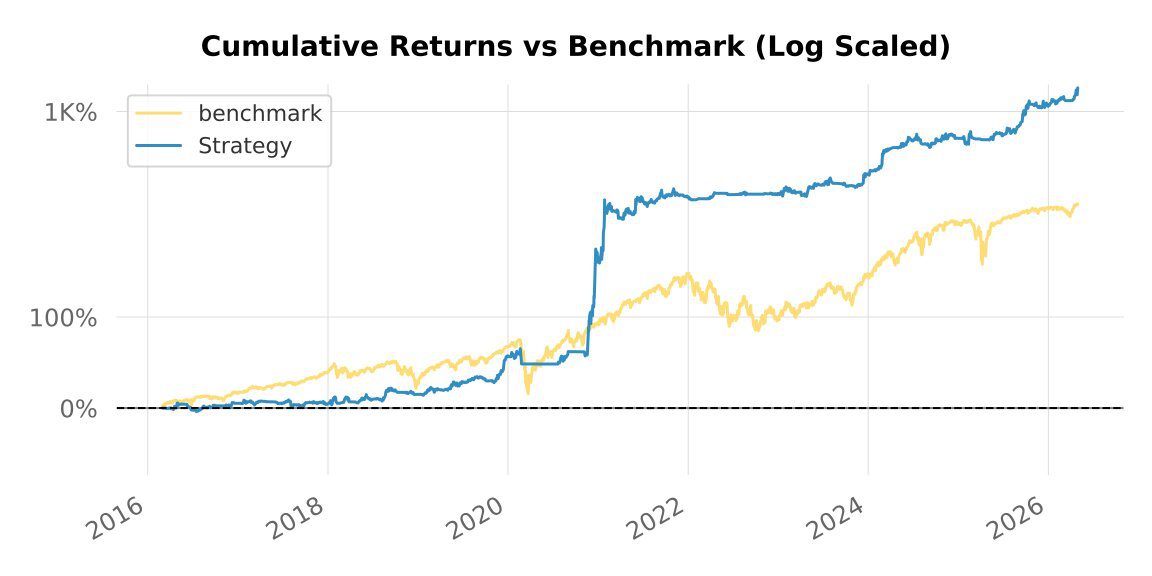

Backtest 317 evaluates a long-only, daily-bar systematic strategy on a broad universe of 4,176 US-listed equities from 1 March 2016 to 30 April 2026 (≈ 10 years 2 months). Over that window the strategy compounds to a CAGR of 30.4% versus the S&P 500 total-return benchmark at 13.8%, with a max drawdown of -17.70% against the benchmark’s -33.92% – while holding positions only 78% of the time.

This is a historical backtest, not a live track record and not a trading signal. Past performance is not indicative of future results. Content is published for informational and educational purposes only – see the closing notes and our community page for the full disclaimer.

Headline numbers

| Metric | Strategy | Benchmark (SPX TR) |

|---|---|---|

| Period | 2016-03-01 → 2026-04-30 | |

| CAGR | 30.41% | 13.80% |

| Cumulative return | +1,394% | +273% |

| Max drawdown | -17.70% | -33.92% |

| Longest DD (days) | 448 | 745 |

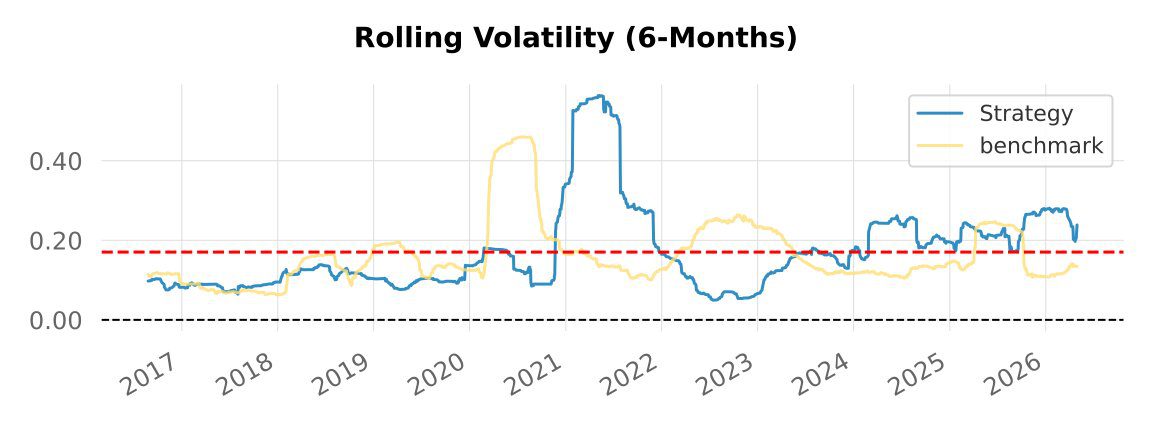

| Volatility (annualised) | 20.30% | 17.93% |

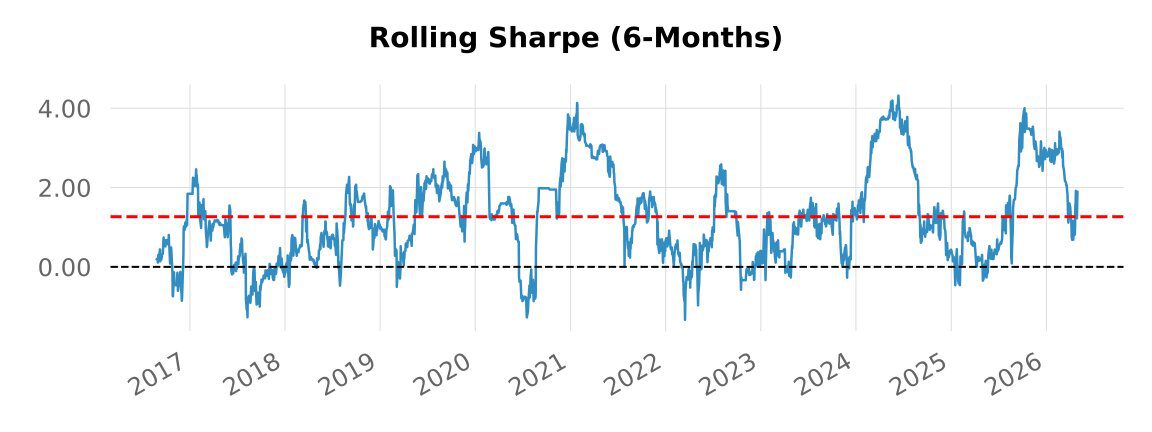

| Sharpe | 0.78 | 0.10 |

| Sortino | 1.35 | 0.14 |

| Calmar | 1.72 | 0.41 |

| Time in market | 78% | 100% |

| Gross exposure (avg) | 36% | – |

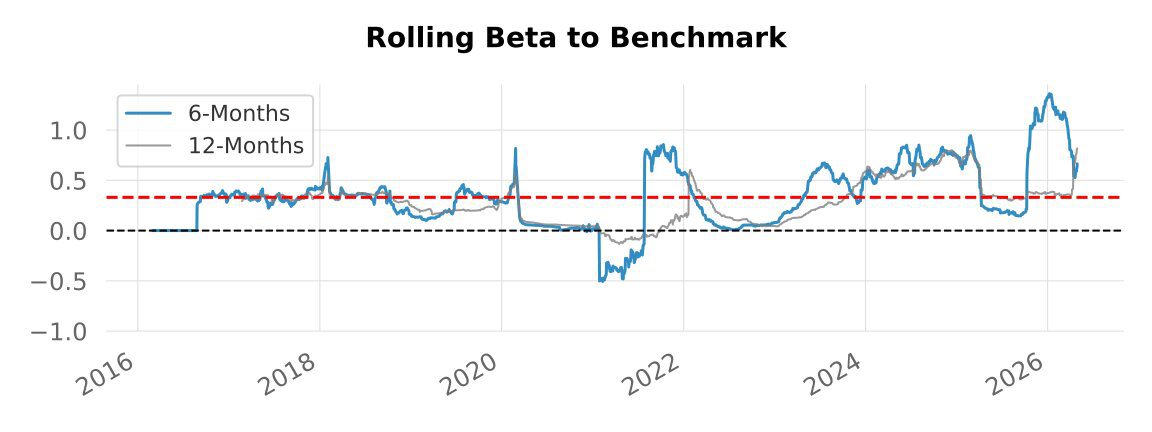

| Beta to SPX | 0.20 | – |

| Trades | 818 | – |

| Win rate | 53.30% | – |

| Risk / reward | 1.75 | – |

| Skew | +3.33 | -0.38 |

| Kurtosis | 57.25 | 16.21 |

Universe & period

The universe is the US-equities zone – 4,176 US-listed stocks, daily bars, denominated in USD. This is a much wider cross-section than our world major-index studies, which changes the character of the strategy: with thousands of candidates the entry logic can be selective, and average gross exposure sits around 36% with the book in the market only 78% of the time. The simulation warms up indicators from 2014-12-19 and starts compounding from 2016-03-01 with $100,000 of initial capital, ending 2026-04-30.

Strategy in plain English

- Long-only, no shorts, no leverage.

- Entry: a MACD-variant trigger (internally

macdv3b). - Exit: a composite of a moving-average rule and a VIX-based filter (internally

ma0a+vix0b), combined with a 14% trailing stop. - Sizing: volatility-targeted at the portfolio level, position cap 20%, sector cap 33%, max 10 new entries per bar.

- Cooldown: a freeze of 2 bars after each exit to avoid immediate re-entries.

- Regime awareness: a 252-bar percentile-based regime filter. Over the test window bars classify as ~78% trend, ~8% range, ~15% bear (see our follow-up null-result study on whether this filter actually improves backtest outcomes) – the strategy is permitted in all three but sizes down outside trend.

Equity curve

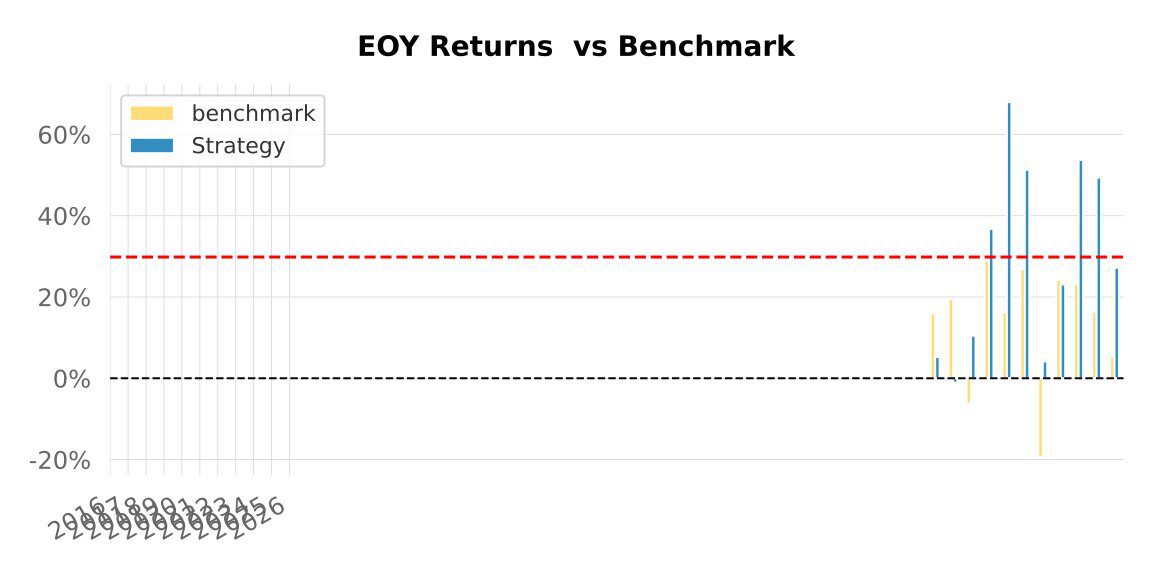

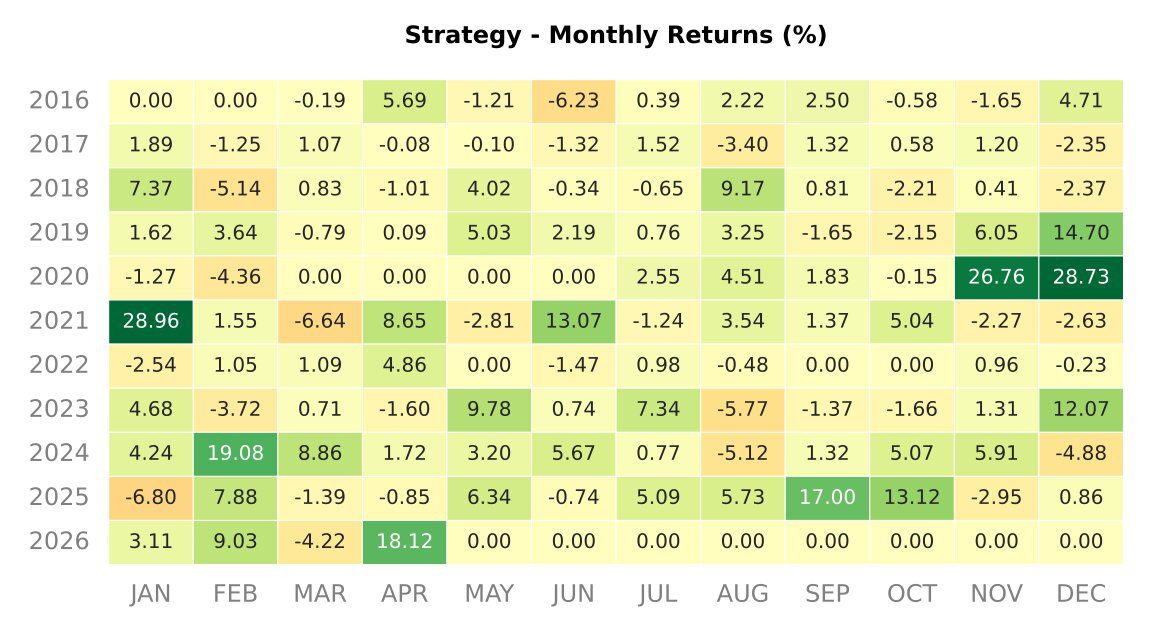

Annual returns

| Year | SPX | Strategy | Multiplier | Won |

|---|---|---|---|---|

| 2016 | 15.87% | 5.22% | 0.33 | – |

| 2017 | 19.42% | -1.06% | -0.05 | – |

| 2018 | -6.24% | 10.46% | -1.68 | + |

| 2019 | 28.88% | 36.71% | 1.27 | + |

| 2020 | 16.26% | 67.92% | 4.18 | + |

| 2021 | 26.89% | 51.28% | 1.91 | + |

| 2022 | -19.44% | 4.12% | -0.21 | + |

| 2023 | 24.23% | 23.05% | 0.95 | – |

| 2024 | 23.31% | 53.72% | 2.30 | + |

| 2025 | 16.39% | 49.37% | 3.01 | + |

| 2026* | 5.31% | 27.19% | 5.12 | + |

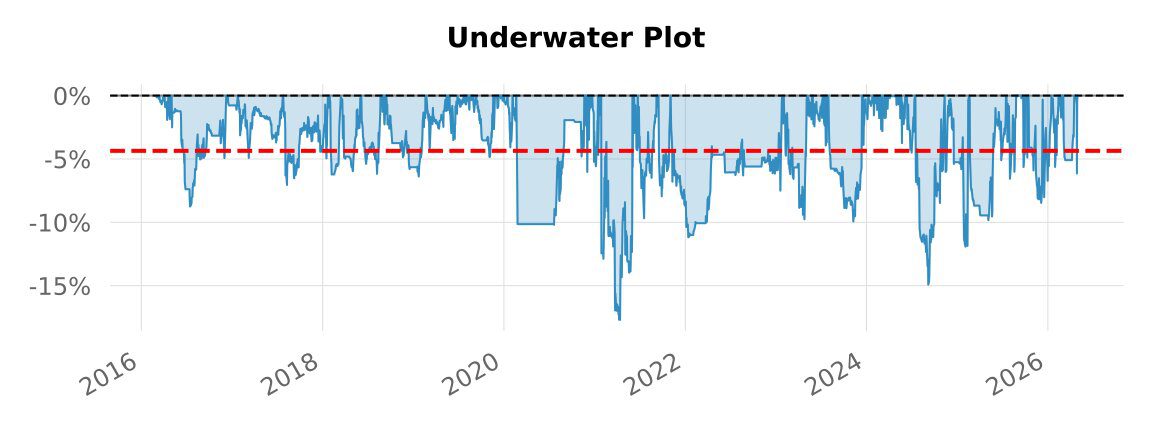

Drawdown analysis

The deepest drawdown sits at -17.70% (Jan-Jun 2021), deeper than our world-index strategies but still roughly half the benchmark’s -33.92% peak-to-trough. The longest underwater stretch ran 448 days through the 2021-2023 chop. All of the worst-ten drawdowns had recovered before the end of the sample – there is no open drawdown in this record.

| Started | Recovered | Drawdown | Days |

|---|---|---|---|

| 2021-01-28 | 2021-06-01 | -17.70% | 125 |

| 2024-07-17 | 2024-11-08 | -14.92% | 115 |

| 2024-11-12 | 2025-02-14 | -11.92% | 95 |

| 2021-11-04 | 2023-01-25 | -11.18% | 448 |

| 2020-02-21 | 2020-11-19 | -10.20% | 273 |

| 2023-08-01 | 2023-12-13 | -9.93% | 135 |

| 2025-02-20 | 2025-07-15 | -9.83% | 146 |

| 2023-02-03 | 2023-05-05 | -9.76% | 92 |

| 2021-06-25 | 2021-09-07 | -9.68% | 75 |

| 2016-05-03 | 2016-12-07 | -8.75% | 219 |

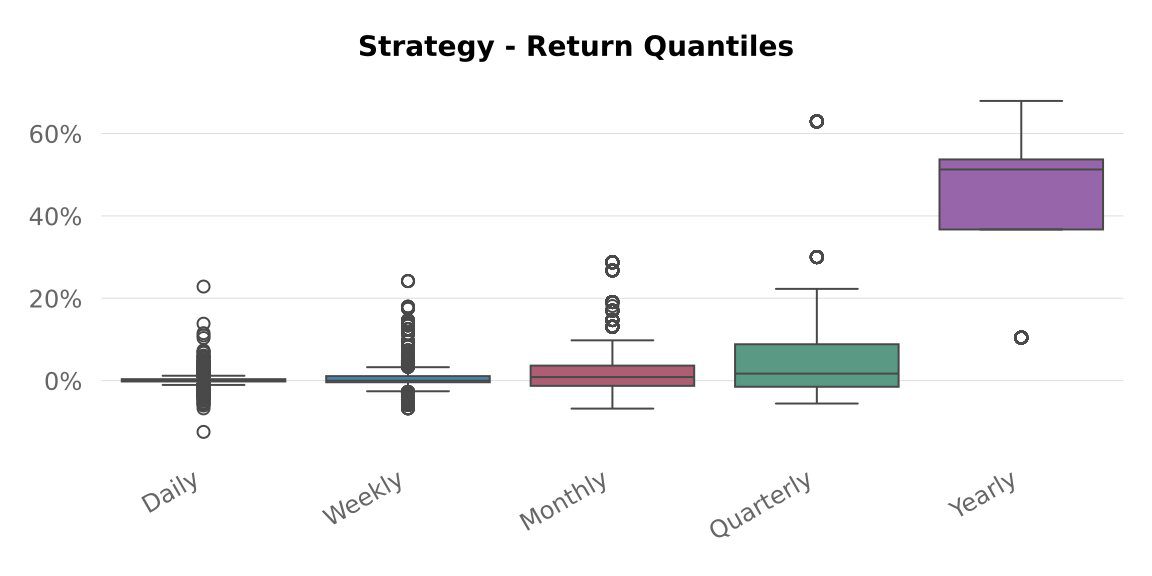

Rolling metrics

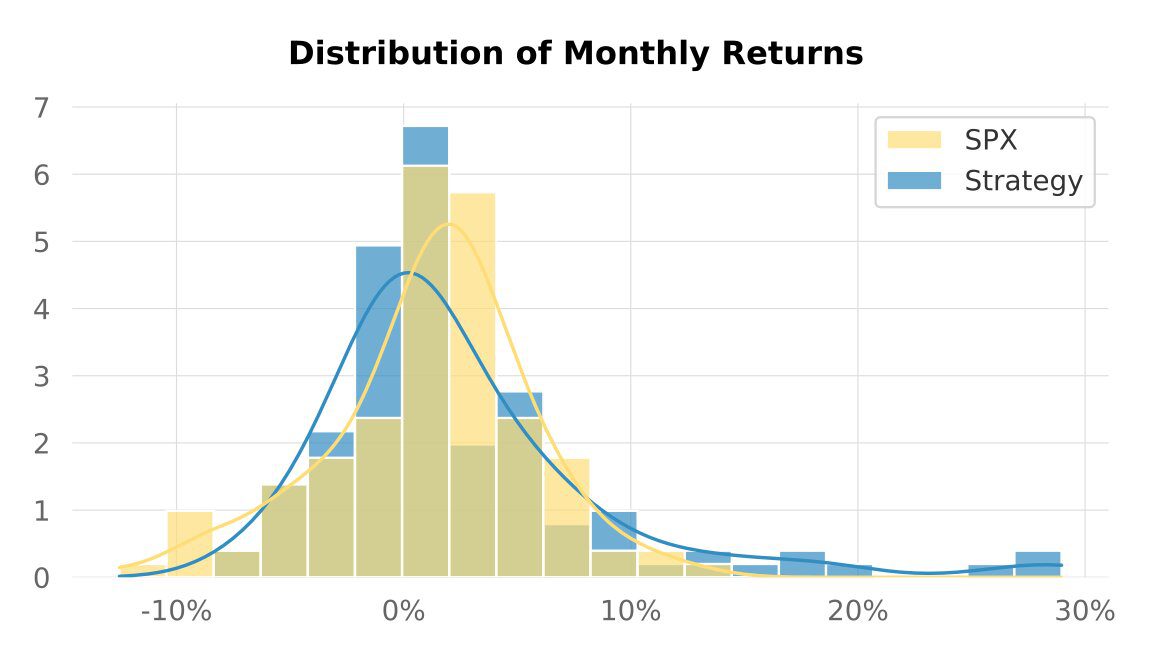

Return distribution

Two distribution stats deserve a flag: skew of +3.33 and kurtosis of 57.25. That is a heavily right-tailed, fat-tailed profile – a relatively small number of very large up-days carry a disproportionate share of the compounding. Positive skew is the friendly direction (the surprises are mostly to the upside), but extreme kurtosis is also a fragility signal: results that lean on a handful of outliers are more sensitive to whether those specific days survive different cost, slippage and universe assumptions. Read the headline CAGR with that in mind.

Caveats & reading guide

- This is a backtest, not a live track record. Trades are simulated on historical daily bars; real-world execution would face additional slippage, partial fills, and venue-specific frictions.

- Outlier-driven distribution. Skew +3.33 and kurtosis 57.25 mean a handful of large up-days do a lot of the work. That is exactly the kind of profile that can degrade under different cost or universe assumptions – treat the CAGR as fragile, not bankable.

- Breadth and liquidity. A 4,176-name US universe includes small and less-liquid stocks. Real fills on the thinner names would be worse than the bar-level model assumes; a liquidity-filtered re-run would be a fairer test.

- Survivorship. The universe is built from current and historical listings; while care is taken to include delisted names, residual survivorship bias cannot be ruled out.

- Risk-free rate. The QuantStats report uses a high annual RF (13.6%, inherited from a working assumption), which mechanically suppresses the printed Sharpe. An RF-flat internal calculation reports Sharpe 0.81, Sortino 1.02 and Calmar 1.69 over the same window.

- Costs. Transaction costs, a value-traded borrow-fee model (0.8%) and a 1.5% margin spread are modelled at the bar level; the strategy turns over ~80 trades per year on average (818 total).

- Out-of-sample. Parameter selection used the early portion of the window; results from 2020 onward give a more honest read of out-of-sample behaviour. The weak 2016-2017 stretch (including a -1.06% year against a +19% market) is part of the honest picture. Hard cutoff: the strategy’s rules and parameters were frozen on 3 July 2025, so all performance after that date is genuine out-of-sample / forward-tracked data – unseen at selection time, with no hindsight possible.

Discuss this backtest

We share backtest research, methodology notes and discussion on our free community channels – Telegram, Discord, X. Full details and the bilingual disclaimer on the community page.

KreamEdge publishes systematic strategy backtests and market analytics for informational and educational purposes only – not personalised investment advice. Past performance is not indicative of future results.

0 Comments